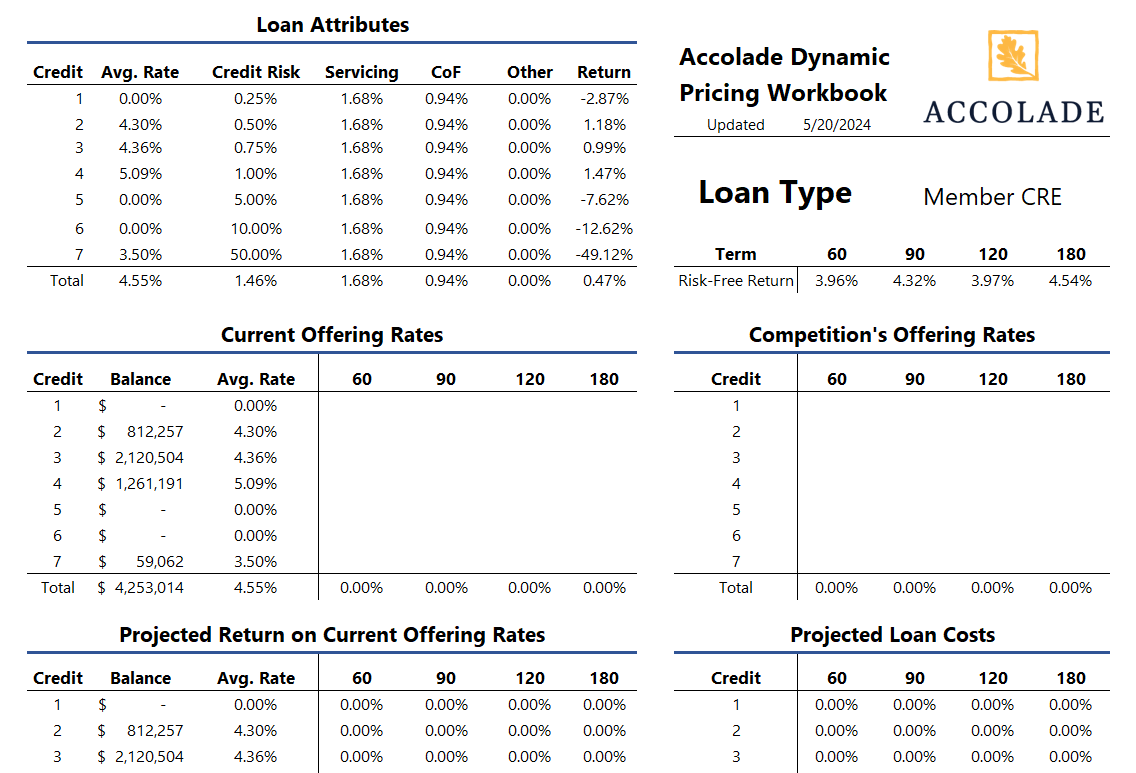

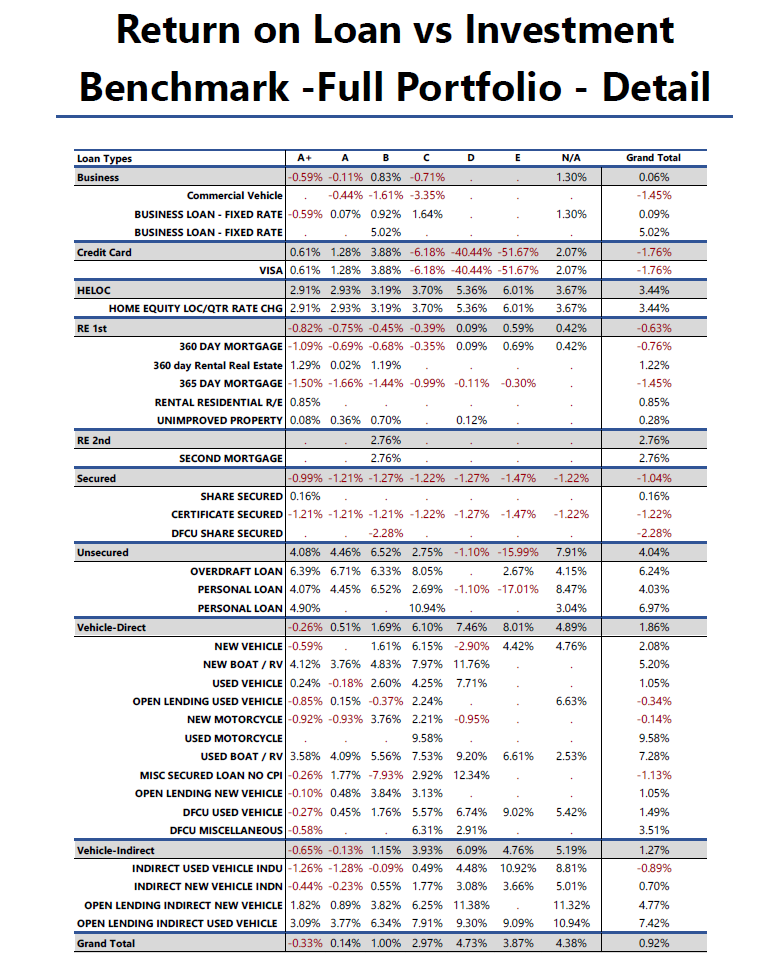

Different types of loans should be evaluated net of expenses and compared to similar investments to evaluate opportunity cost. Once the loan pricing model has determined net yield across credit tiers and product types, we provide customized investment benchmarks to help determine if the loan offering meets strategic guidelines.

If a loan is underpriced management can adjust future pricing or assess the value of obtaining the member relationship. We can choose to make a loan at a lower return, but we had better know why we are doing it.

.png?width=200&height=200&name=lpp%20(1).png "Icon showing data files loading into computer")